Persistent Just Made the Biggest Acquisition in Its History. So why did it plunge 11% in a Day?

Persistent Systems' €1.27 billion bid for Germany's Nagarro should have strengthened its position in Europe. Instead, investors erased nearly the same amount from its own market value in a single trading session. The question isn't whether the deal is strategic. It's whether Persistent paid too much for it.

For most companies, announcing the largest acquisition in their history is usually a reason to celebrate. It signals ambition, opens new markets and tells investors management is thinking beyond the next quarter.

Persistent Systems received the opposite reaction.

On June 29, the company's shares fell 11.22%, closing at ₹4,298.50, after announcing a €1.27 billion ($1.4 billion) all-cash acquisition of German digital engineering firm Nagarro. The selloff wiped out roughly a tenth of Persistent's market value, making it the worst-performing stock on the NIFTY Midcap 100 and pushing it to a near 15-month low.

The market wasn't questioning Persistent's ambition.

It was questioning the price of that ambition.

What the numbers say

The acquisition immediately transforms Persistent into a much larger player across continental Europe.

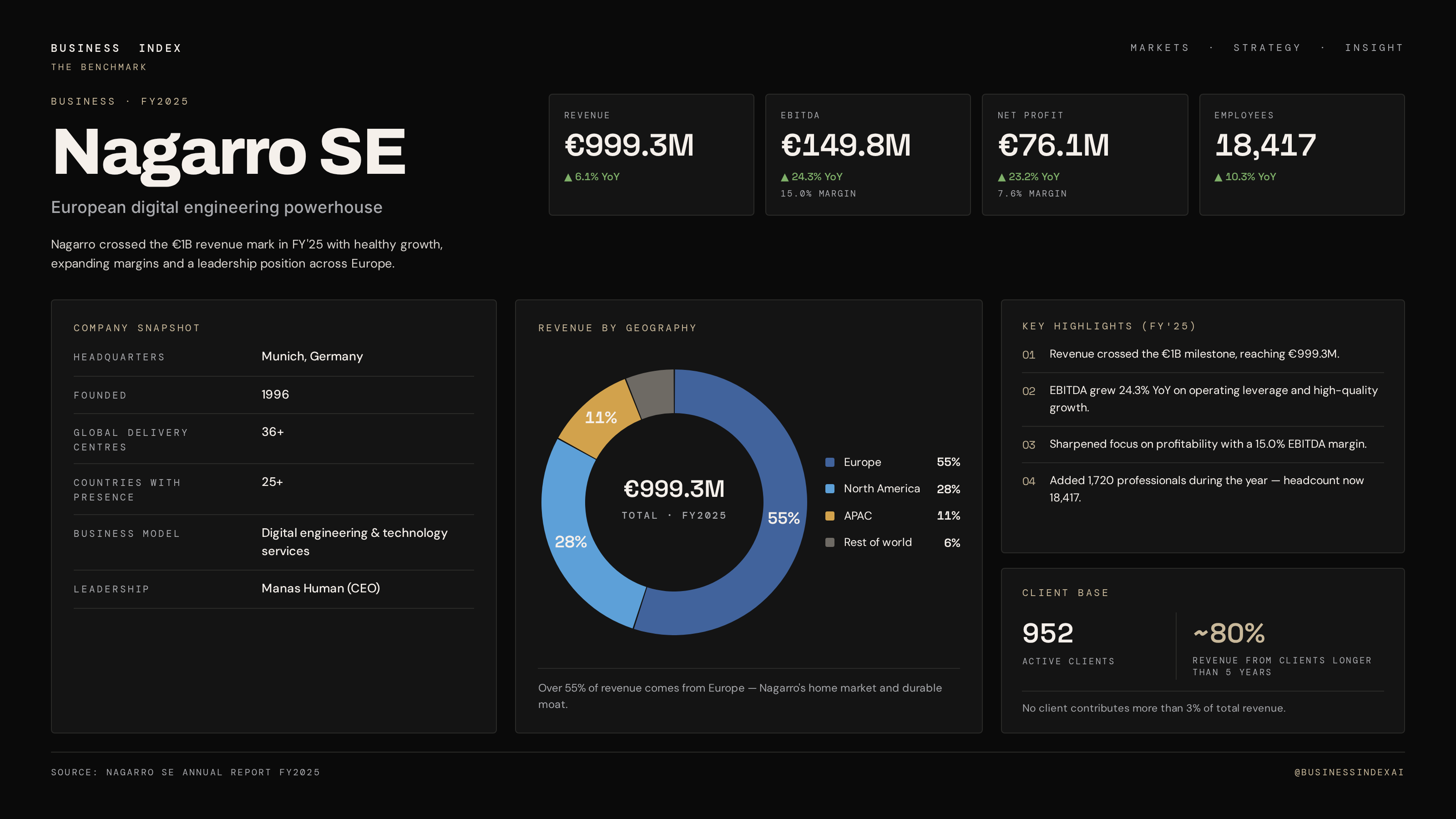

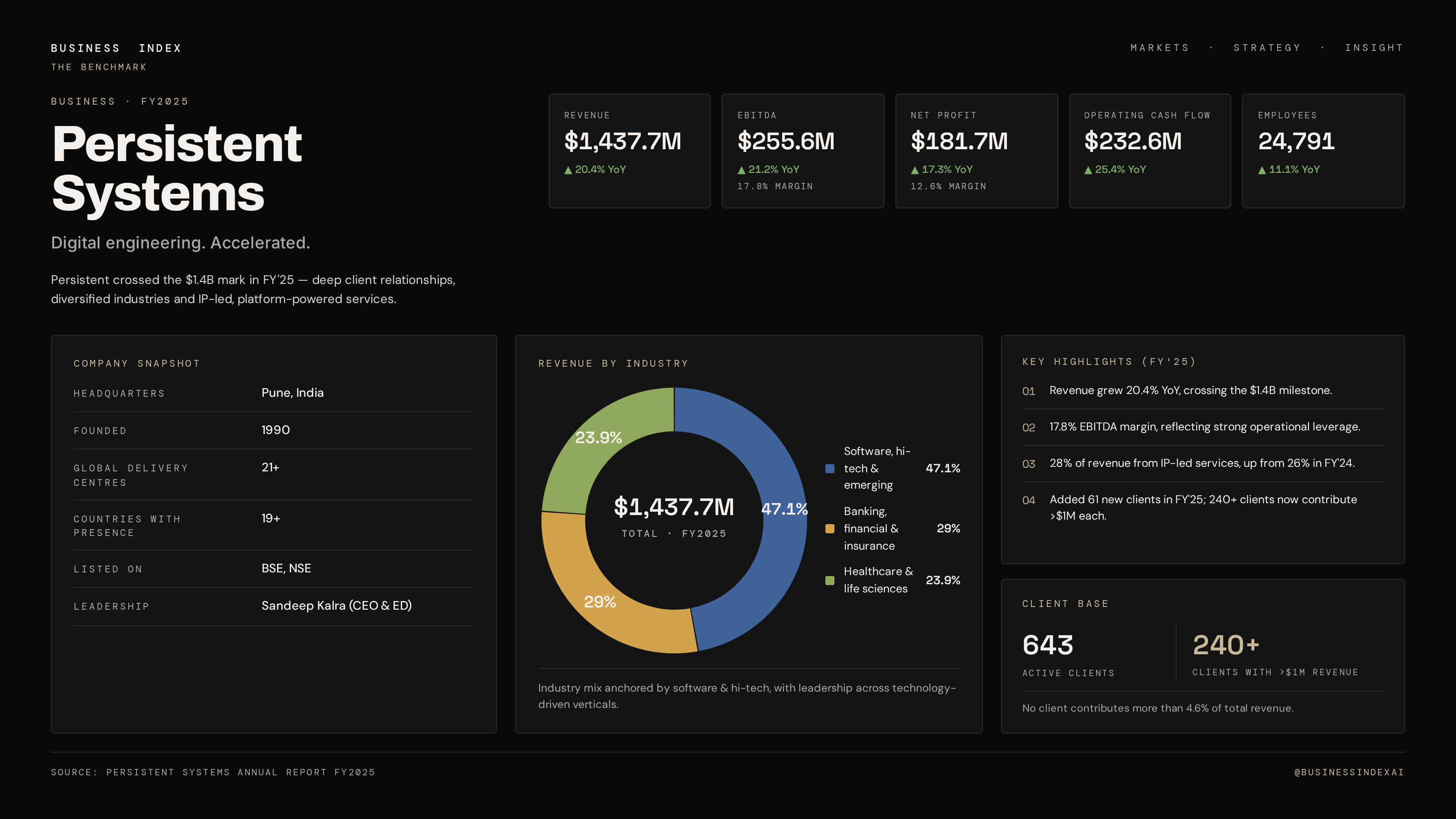

Nagarro brings more than 18,000 employees, deep enterprise relationships across Germany and the Nordics, and stronger capabilities in digital engineering. It is exactly the kind of asset that could help Persistent compete more aggressively with larger Indian IT peers such as TCS, Infosys and Wipro.

Strategically, the logic is easy to understand.

Financially, investors see a more complicated picture.

Persistent is paying a 140% premium over Nagarro's June 25 closing price on the Frankfurt Stock Exchange and roughly 94% above its three-month volume-weighted average price.

Those numbers immediately raised questions.

Large acquisition premiums are usually justified when a target possesses exceptional technology, dominant market share or unusually high profitability. Investors are not yet convinced Nagarro checks enough of those boxes.

For the market, this wasn't just an acquisition.

It was a very expensive acquisition.

The margin problem

Growth is only valuable if it creates shareholder value.

One of the Street's biggest concerns is profitability.

Nagarro operates at structurally lower margins than Persistent. While the acquisition significantly increases revenue, analysts expect it to dilute the combined company's profitability, at least in the near term.

Several brokerages estimate the transaction could reduce gross margins by roughly 120 basis points and EBITDA margins by as much as 200 basis points before integration benefits begin to materialise.

That means Persistent could become a larger company while temporarily becoming a less profitable one.

Markets rarely reward that trade-off.

Debt changes the equation

The acquisition is also being financed through a bridge loan.

That immediately increases leverage and introduces another layer of execution risk.

Cross-border acquisitions in technology are rarely straightforward. Different operating cultures, overlapping delivery teams, client retention and regulatory approvals all create uncertainty during integration.

Even well-managed acquisitions often take years before promised synergies begin appearing in financial statements.

Investors know that.

Which explains why many preferred to sell first and wait for evidence later.

The Street isn't unanimous

Not every analyst believes the market reaction was justified.

CLSA maintained a High Conviction Outperform rating, arguing the acquisition strengthens Persistent's long-term strategic position and accelerates its expansion in Europe.

Others remain more cautious.

Nomura initiated coverage with a Neutral stance, acknowledging the strategic rationale while highlighting execution challenges.

Elara Capital retained its Sell recommendation, citing valuation concerns, margin dilution and integration risk.

The divergence itself tells an important story.

Everyone agrees the acquisition is transformative.

They disagree on whether shareholders are paying too high a price for that transformation.

Why this matters

Persistent has quietly become one of India's best-performing mid-cap technology companies over the past five years.

Unlike many IT peers, it consistently delivered faster growth, stronger execution and better capital allocation. That track record earned management significant credibility with investors.

The Nagarro acquisition is the company's boldest move yet.

Success would immediately strengthen Persistent's presence across Europe, expand its enterprise customer base and reposition it as a larger global digital engineering company.

Failure would leave shareholders with lower margins, higher debt and an acquisition premium that becomes increasingly difficult to justify.

That is why the market reacted so sharply.

Investors are not voting on today's announcement.

They are pricing tomorrow's execution.

What to watch

- Regulatory approvals across Germany and other jurisdictions.

- Management's integration roadmap during the next earnings call.

- Updated margin guidance for FY27.

- Client retention across Nagarro's enterprise accounts.

- Any indication of cost synergies or cross-selling opportunities.

- Debt reduction plans following the acquisition.

The closing thought

Markets often punish uncertainty more than bad news.

Persistent has made the biggest strategic bet in its history.

The acquisition itself may prove successful.

But after paying one of the steepest premiums seen in recent Indian IT M&A, management now faces a different challenge.

It doesn't just have to integrate Nagarro.

It has to convince investors that the price was worth paying.

One email. Saturday morning.

The week that mattered.

The five stories you needed to read, the data point of the week, and what to watch. From the Business Index editors. No ads, no fluff.