Revenue scaled from FY24 to FY26, but adjusted EBITDA remained deeply negative. Source: Zepto UDRHP-I.

Photo · Zepto revenue and adjusted EBITDA chart

Zepto’s IPO is a public-market test of speed, scale... & burn?

Zepto is not coming to market as a normal consumer company. It is asking investors to value a new retail habit before the profit pool has been proven.

That distinction matters. The UDRHP does show a company with real scale. Zepto processed 640.18 million orders in FY26, up from 332.11 million in FY25 and 132.87 million in FY24. It ended FY26 with 1,139 dark stores, 47.97 million annual transacting users and ₹22,623.58 crore of revenue from operations. Those are not vanity metrics. They show that quick commerce has moved from a Bengaluru-Mumbai-Delhi convenience story into a national urban retail format.

The same filing also shows the cost of creating that habit. Adjusted EBITDA was negative ₹5,041.55 crore in FY26, against negative ₹4,521.69 crore in FY25 and negative ₹1,124.59 crore in FY24. Restated loss for the year was ₹5,905.19 crore. Free cash flow was negative ₹4,329.54 crore. Zepto is improving some unit metrics, but the company is still consuming cash at a scale that public investors will have to underwrite.

What the numbers say

The headline IPO structure is straightforward. Zepto is proposing a fresh issue of up to ₹8,010 crore and an offer for sale of up to 113,466,566 equity shares by existing shareholders. Reuters reported the issue as a raise of up to $837 million, with proceeds intended for dark-store expansion, technology and cloud infrastructure, and acquisitions.

The fresh issue is not small. It is roughly 1.36 times Zepto’s FY26 restated loss. That ratio is the first real filter for investors. This is not an IPO where the company is merely giving early investors liquidity. It is a financing event for a business that still needs capital to expand its network, lease infrastructure, build supply-chain systems and defend its customer base.

The profit-and-loss statement is more revealing than the IPO size. Revenue from operations rose from ₹4,454.52 crore in FY24 to ₹11,109.95 crore in FY25 and ₹22,623.58 crore in FY26. Adjusted EBITDA moved from negative ₹1,124.59 crore to negative ₹4,521.69 crore and then negative ₹5,041.55 crore across the same period. Revenue grew 103.63% in FY26. Adjusted EBITDA loss widened by 11.5%.

That is progress, but not proof. Zepto’s adjusted EBITDA as a percentage of net receivables value improved from negative 35.59% in FY25 to negative 20.32% in FY26. Adjusted EBITDA per order improved from negative ₹136.15 in FY25 to negative ₹78.75 in FY26. Those metrics say the machine is getting more efficient. They do not yet say the machine is profitable.

The operating engine is equally important. Total orders rose 92.8% in FY26 to 640.18 million. Orders per day rose to 1.75 million. The store network went from 337 dark stores at the end of FY24 to 1,029 in FY25 and 1,139 in FY26. Orders per store per day rose to 1,677 in FY26, from 1,565 in FY25 and 1,325 in FY24.

That combination is the best argument for the IPO. Zepto is not merely opening stores and hoping demand appears. More orders are passing through each store. Scale is improving local productivity. The company is also generating a meaningful advertising business: advertisement revenue rose from ₹49.17 crore in FY24 to ₹651.24 crore in FY25 and ₹1,635.73 crore in FY26.

But user growth tells a more cautious story. Annual transacting users rose from 10.57 million in FY24 to 38.38 million in FY25 and 47.97 million in FY26. That is strong. Yet quarterly data in the UDRHP shows ATU slipping from 49.54 million in December 2025 to 47.97 million in March 2026. That one-quarter drop does not kill the story. It does show that order growth and user growth are no longer moving with equal force.

“we have incurred losses and negative cash flows from operating activities since our inception” - Zepto Limited UDRHP-I, Jun. 8, 2026.

The ownership signal

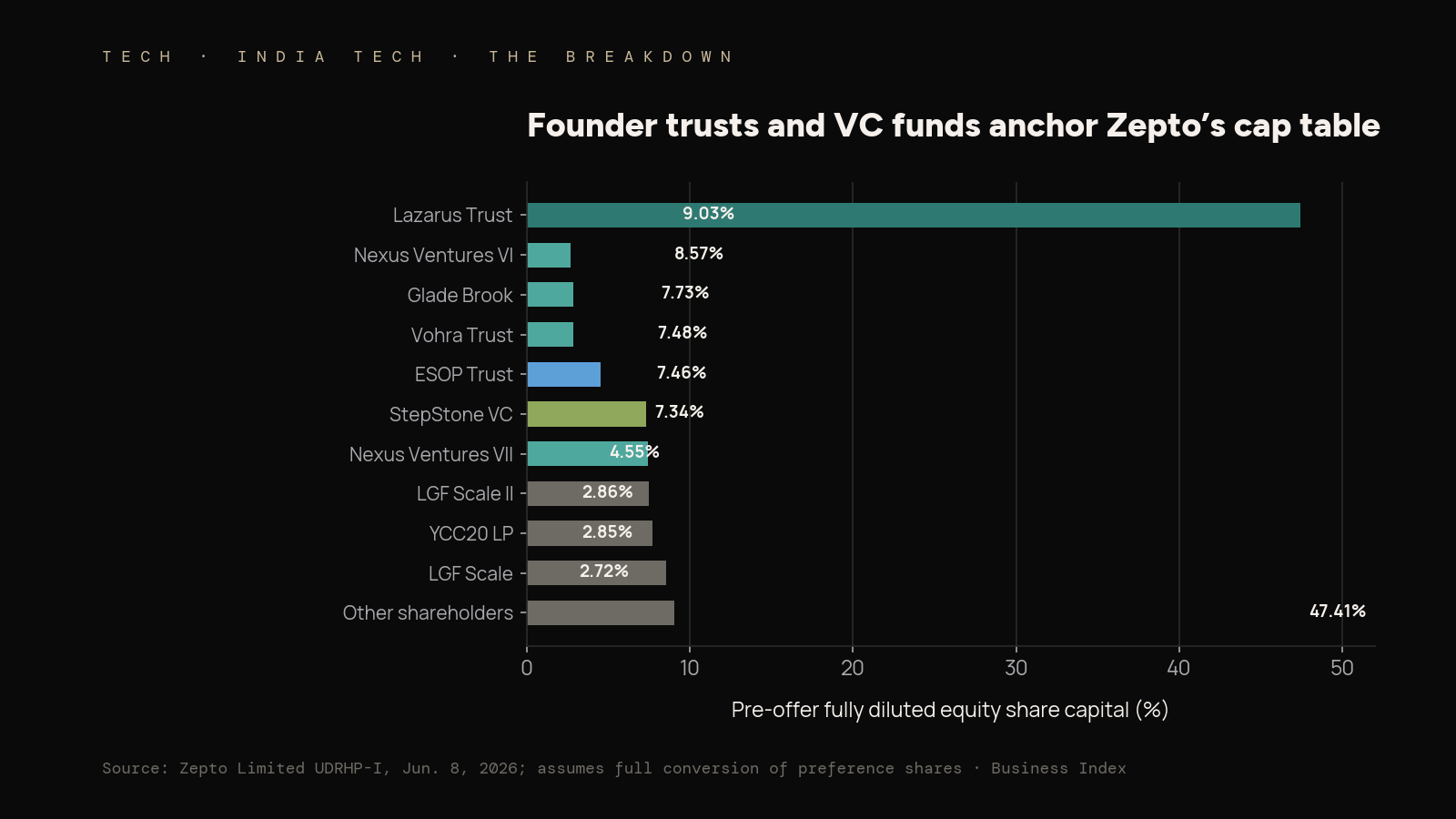

Zepto’s cap table is unusually broad for a consumer company heading to market. The UDRHP says the company had 5,895 shareholders as on the date of the updated filing, including 4,247 equity shareholders and 1,824 preference shareholders. On a fully diluted pre-offer basis, the largest disclosed shareholders are founder-linked Lazarus Trust at 9.03%, Nexus Ventures VI at 8.57%, Glade Brook Private Investors XXXIV at 7.73%, The Vohra Trust at 7.48%, the Zepto Employee Stock Option Trust at 7.46% and StepStone VC Zepto at 7.34%.

That ownership structure cuts both ways. It avoids an overconcentrated founder cap table. It also means public investors are buying into a company where several private-market investors already have a route to liquidity.

The offer-for-sale portion confirms the point. Selling shareholders include Nexus Ventures VI, Nexus Ventures VII, Contrary ZEP Holdings, Razor Ventures Zepto, Kaiser Foundation Hospitals and Kaiser Permanente Group Trust. Nexus Ventures VI can sell up to 57.36 million shares. Nexus Ventures VII can sell up to 30.40 million shares. Razor Ventures Zepto can sell up to 9.36 million shares. Contrary ZEP Holdings can sell up to 7.80 million shares.

Founders Aadit Palicha and Kaivalya Vohra are the public face of the company, but the shareholder economics are already institutional. That is normal for a late-stage venture-backed company. It still matters for the IPO narrative. A clean founder-retention story is useful. A meaningful OFS by venture funds is equally real. Both can be true.

The more interesting number is not the individual founder line. It is the founder-trust line. Lazarus Trust and The Vohra Trust together account for 16.51% of the pre-offer fully diluted equity share capital in the major shareholder table. Including Aadit Palicha’s direct 1.07% disclosed in that table takes the visible founder-linked holding to 17.58%, before considering holdings below the 1% disclosure threshold.

For a public investor, this means the incentive structure is not broken. The founders and their trusts remain material. But the listing is also a liquidity window for the venture stack that financed the land-grab.

The real quick-commerce question

The quick-commerce debate is often framed as a customer question. Will people keep ordering milk, fruit, beauty products and phone chargers in 10 minutes once discounts fade? Zepto’s filing suggests the better question is operational.

Can the company push enough order density through each dark store to make the network profitable before the market demands lower burn?

The store metrics say there is operating leverage. Closing stores rose only 10.7% in FY26, from 1,029 to 1,139. Total orders rose 92.8%. That is why orders per store per day improved. It means the existing network carried more throughput instead of every increment of order volume needing an equivalent increment of real estate.

The difficulty is that throughput alone is not enough. Quick commerce is a three-sided cost problem: inventory economics, fulfilment economics and delivery economics. Zepto does not own every piece of inventory in the way a conventional retailer would; the model involves merchant partners and dark-store services. But the network still has to bear people, leases, technology, supply-chain coordination, delivery capacity and customer acquisition.

That is where the missing disclosures matter. Moneycontrol pointed out that the IPO document omits some operating metrics public-market investors usually want for a consumer platform: contribution margins, average order values and monthly transacting users. The UDRHP gives total orders, annual transacting users, orders per day, stores and adjusted EBITDA per order. That is a useful set. It is not the full set.

Without average order value and contribution margin by cohort, investors cannot easily separate a good order from a subsidised order. Without monthly user metrics, they cannot fully assess churn and reactivation. Without mature-store economics, they cannot know whether a dense store becomes structurally profitable after crossing a threshold, or whether the platform merely loses less money as volume rises.

The annual data points toward improvement. The March-quarter data, reported by Moneycontrol, is more favourable: revenue rose 75% year on year to ₹7,497.64 crore, total orders reached 210 million, average daily orders rose to 23.3 lakh, stores reached 1,139 and orders per store per day increased to 2,140 from 1,425 a year earlier. Adjusted EBITDA loss per order also narrowed in the March quarter.

That quarter is important because it is what the IPO will sell. Investors are not buying FY24. They are buying the claim that the FY26 exit rate is closer to the future shape of the business. The problem is that the annual cash-flow statement still carries the weight of the build-out.

The regulatory overhang

The UDRHP also discloses a regulatory risk that should not be dismissed as routine. The Enforcement Directorate issued summons to Aadit Palicha and Kaivalya Vohra in April 2026 under the Foreign Exchange Management Act. The founders were asked for information including foreign investments, shareholding pattern, loans or guarantees, income tax returns and bank accounts. Reuters reported that the company said the founders complied and had received no further communication as of the filing date.

This is not the centre of the investment case. It is a risk factor. But public markets treat unresolved regulatory questions differently from private markets. A private round can absorb ambiguity if lead investors are comfortable with the documents. A listed stock has daily price discovery. Any fresh communication from the ED after listing would become a market event.

Zepto’s best defence is disclosure. The summons are in the UDRHP. The request was complied with. The company says no further communication had been received as of the filing date. That does not remove the risk. It defines it.

Why this matters

Zepto is the first clean public-market test of pure-play Indian quick commerce. Eternal gives investors Blinkit inside a wider food-delivery and platform company. Swiggy gives investors Instamart inside a broader consumer-internet stack. Zepto is the sharper instrument.

That makes the listing more useful and more dangerous. Useful, because it gives public markets a direct way to price the quick-commerce model. Dangerous, because there is nowhere to hide if the model disappoints. Revenue growth can no longer be enough. The company will have to show that store density, higher frequency, advertising revenue and operating discipline can reduce burn without handing customers to Blinkit, Instamart, Amazon, Flipkart or BigBasket.

The central contradiction is visible in the UDRHP. Zepto has the scale of a public company and the cash profile of a company still being built. It processed 640 million orders in a year. It also used ₹3,462.44 crore of cash in operating activities and generated negative free cash flow of ₹4,329.54 crore.

The IPO will therefore be less about whether Indians like quick commerce. That question has already been answered. The question is whether public investors will accept the economics required to deliver it.

What to watch

- Final offer size and whether the OFS component grows or shrinks before the red herring prospectus.

- Any change in disclosed valuation range versus Zepto’s last private valuation of around $7 billion.

- Mature-store contribution margin, if management starts disclosing it in roadshows or listed quarterly updates.

- March-quarter unit economics, especially adjusted EBITDA per order and orders per store per day.

- The ED disclosure and whether any further communication is received after the UDRHP date.

- The competitive response from Blinkit, Instamart, Amazon, Flipkart and BigBasket during the IPO marketing window.

Zepto’s IPO will not price delivery speed. It will price how much burn public markets are willing to forgive for proof that speed has become a habit.

Sources

- SEBI. Zepto Limited - UDRHP1 filing page. https://www.sebi.gov.in/filings/public-issues/jun-2026/zepto-limited-udrhp1_101929.html

- Axis Capital / Zepto. Zepto Limited - UDRHP-I PDF. https://www.axiscapital.co.in/contents/Zepto%20Limited%20-%20UDRHP-I-1780938548.pdf

- Reuters. Indian quick commerce firm Zepto to raise up to $837 million in IPO. https://www.reuters.com/world/india/indian-quick-commerce-firm-zepto-raise-up-837-million-ipo-2026-06-08/

- Moneycontrol. Zepto's Q4 revenue jumps 75% YoY to Rs 7,498 crore. https://www.moneycontrol.com/news/business/startup/zepto-s-q4-revenue-jumps-75-yoy-to-rs-7-498-crore-adjusted-ebitda-loss-narrows-ahead-of-ipo-13944222.html

- Moneycontrol. Missing metrics: Zepto IPO document omits contribution margins, order values, monthly transacting users. https://www.moneycontrol.com/news/business/startup/missing-metrics-zepto-ipo-document-omits-contribution-margins-order-values-monthly-transacting-users-13948011.html

- Inc42. Zepto FY26: Loss jumps 26% YoY to ₹5,905 Cr, revenue doubles. https://inc42.com/buzz/zepto-fy26-loss-jumps-26-yoy-to-%E2%82%B95905-cr-revenue-doubles/

One email. Saturday morning.

The week that mattered.

The five stories you needed to read, the data point of the week, and what to watch. From the Business Index editors. No ads, no fluff.